-

86-21-63895588

86-21-63895588

-

No.1, Lane 600, Nanchezhan Road, Huangpu District, Shanghai 200011

No.1, Lane 600, Nanchezhan Road, Huangpu District, Shanghai 200011

Release time:2023-11-16

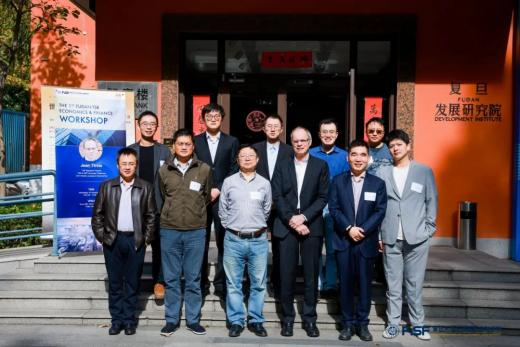

On November 8th 2023, the 1st “Fudan-TSE Economics & Finance Workshop” was successfully held in the Think Tank Building, Handan Campus, Fudan University. Yongqin Wang, Distinguished Professor of FISF, Huasheng Gao, Deputy Dean of FISF, Deputy Secretary of General Party Branch and Professor in Finance, Zhiyuan Li, Deputy Director Professor of Department of World Economics, School of Economics, Fudan University, Yi Huang, Professor in Finance at Fudan University, Bo Hu, Lecturer of School of Economics, Fudan University, and Yifan Zhou, Assistant Professor at FISF, respectively made keynote speeches. Jean Tirole, Winner of the 2014 Nobel Prize in Economics and Professor of TSE, was invited to attend the seminar and make careful comments on the speech contents.

The first half of the meeting was held by Xiaxin Wang, Associate Professor in Economics at FISF.

Professor Yongqin Wang giving his keynote speech

Yongqin Wang, a Professor of the School of Economics, Fudan University and a Distinguished Professor of FISF, gave a keynote speech entitled Information Sensitivity of Treasury Bonds and Stocks to share his latest research in cooperation with Tri Vi Dang and Wei Li, which expanded the bond information sensitivity theory to the market where investors could sell securities before their maturity and proposed an empirical method to measure information sensitivity. According to the research result, the long-term treasury bonds in the US as safe assets have information sensitivity as high as the S&P 500 index. The article also presented the information sensitivity channels for government (or central bank) asset purchases or commitments. During the collapse of the Chinese stock market in 2015, the information sensitivity of the stocks purchased by the "national team" decreased by 16% (compared to other stocks); and when the stock information sensitivity decreased, the information offered by financial analysts also decreased. To a large extent, a financial crisis is often an information event; the information sensitivity theory and the empirical measurement depict a feature of securities triggering information production, which, unlike traditional risk measurements (no rank correlation exists between them), applies to the research on liquidity risks and financial fragility in financial markets and shall be taken as a new pricing factor.

Professor Huasheng Gao giving his keynote speech

In the keynote speech entitled The Value of Anonymity in Social Media: Evidence from the Stock Market, Professor Huasheng Gao, Deputy Dean of FISF, Deputy Secretary of the General Party Branch and a Professor in Finance, analyzed the value and significance of the research on anonymity in social media in the context of the stock market. With the change in China’s regulatory policies, social media has done away with anonymity and required real-name registration, which research has found to have led to a sharp decline in corporate value, especially when investors are more reliant on social media to acquire stock information. In addition, it is further stated in the research that such policy caused a decrease in stock price information, an increase in the risk of the stock market crash, insufficient company disclosure and more earnings manipulation. Overall, the research offers evidence to prove that canceling anonymity in social media can reduce corporate value by worsening the environment of company information.

Professor Zhiyuan Li giving his keynote speech

Subsequently, Professor Zhiyuan Li, Deputy Director Professor of the Department of World Economics, School of Economics, Fudan University, delivered a keynote speech entitled The Endogenous Intensity of Modular Production and Comparative Advantages. In the speech, he proposed an endogenous method to identify the intensity of comparative advantages, offering a supplement to the classical Ricardo-style international trade theory. Research shows that the scale of the production module determines the intensity of a country’s comparative advantages. Cutting down the module scale or refining the module can release the comparative advantages restricted in the bundled production of a larger module, as countries with comparative advantages in sub-modules must be bundled with other countries with comparative advantages to conduct international trade. Refined modules can enhance comparative advantages, and thus complement trade liberalization in generating welfare gains. Therefore, the theory set up by Professor Zhiyuan Li together with his cooperators associates modular production with the intensity of comparative advantages, which is conducive to understanding certain trade gains and figuring out how to realize division of labor and how to develop comparative advantages in a more general way.

The second half of the meeting was held by Chang Ma, Associate Professor in Finance at FISF.

Professor Yi Huang giving his keynote speech

Yi Huang, a Professor in Finance at Fudan University, gave a speech entitled Fintech Credit and Growth, in which he shared his latest research on fintech. Based on the credit line provided by around two million suppliers trading on e-commerce platforms, Professor Yi Huang and his cooperators found that fintech credit can help promote the sales growth, trade growth and client satisfaction of suppliers. For suppliers under greater impact of information asymmetry and with less collateral, such impacts are more evident. The research reveals the information advantage of fintech credit over traditional credit technology.

Lecturer Bo Hu giving his keynote speech

Bo Hu, Lecturer of the School of Economics, Fudan University, gave a keynote speech entitled Financial Modules in Supply Chain and reported the theoretical research on supply chain finance conducted by him together with his cooperators. With fintech advancing, supply chain finance (reverse factoring) has made remarkable progress. The research aims to capture the four major features of supply chain finance projects in the real world, including: (1) Supply chain finance is typically initiated by one enterprise as the core and involves the participation of thousands of heterogenous suppliers; (2) The core enterprise examines and selects the participating suppliers to improve the profitability and financial conditions in the whole supply chain; (3) The core enterprise acquires higher liquidity by extending the account periods; and (4) Suppliers acquire liquidity by discounting the accounts receivable. In the benchmark model, suppliers are faced with liquidity shock while the core enterprise evaluates the suppliers from two perspectives of liquidity: demand and profitability. The research has drawn a major conclusion that the core enterprise should adopt the strategy of “cross-subsidization for liquidity” to maximize profits, which is to say, backing up suppliers with positive profitability but in need of liquidity support with the positive liquidity contributions of those with negative profitability. Of course, to what extent cross-subsidization shall be applied depends on the self-owned capital of the core enterprise and the shadow value of liquidity in this system. For example, if the core enterprise has contributed a relatively large amount of capital, making liquidity no more significant, the optimal scheme is to focus on suppliers with positive profitability. Professor Bo Hu and his cooperators built the aforementioned benchmark model into the standard framework for the search monetary model and identified the direct influence of the nominal interest rate on the core enterprise’s choice of liquidity and profitability through shadow value. For welfare analysis, the research discovered that supply chain finance, though able to improve social welfare, might generally fail to reach the social optimum. For monetary policies, as cross-subsidization for liquidity can sponsor more suppliers, the zero nominal interest rate (i.e. the Friedman rule) that cannot generate cross-subsidization is not always optimal.

Professor Yifan Zhou giving his keynote speech

In the speech entitled Ownership Concentration and Crisis Recovery, Yifan Zhou, Assistant Professor at FISF, talked about the influence of ownership concentration on company revivals after the global financial crisis (GFC) in 2008-09. It is found that over the ten years after GFC, the excess return on stock price, return on assets, sales growth, Tobin Q, and asset turnover for the companies with higher ownership concentration during GFC have seen a more rapid recovery and growth. Therefore, Professor Yifan Zhou and his cooperators further speculated that the reason might come from outside block holders (non-executive shareholders holding over 5% of the shares), so they focused their research on these outside block holders, expecting to determine that during GFC, companies with a higher concentration of outside block holders might (i) be more likely to vote against the proposals initiated by the company senior management, (ii) appoint a new independent board director and CEO at a higher rate, and (iii) issue less net debt and equity. On this basis, they expected to conclude that such decisions made during financial crises all have a significant effect on the post-crisis revival of the companies.

Jean Tirole

Professor Jean Tirole giving comments

Jean Tirole, Winner of the 2014 Nobel Prize in Economics and Professor of TSE, gave meticulous comments on the contents of all the speeches, providing precious academic advice for young scholars at Fudan and helping them constantly improve their research results. At the seminar, everyone took an active part in the discussion of hot financial topics and economic situations, contributing to the thick academic sharing atmosphere. Through in-depth exploration and mutual learning, the seminar has achieved great results and injected new forces into academic progress and development.

Special thanks to the International Cooperation and Exchange Department of Fudan University for its strong support for this activity!

86-21-63895588

No.1, Lane 600, Nanchezhan Road, Huangpu District, Shanghai 200011

86-21-63895588

No.1, Lane 600, Nanchezhan Road, Huangpu District, Shanghai 200011